The skyrocketing expense of medical care has made having health insurance essential in the modern world. With the number of diseases we face and the unhealthy lifestyle we lead, this is the most effective way to manage the ever-increasing costs of healthcare. Thus, it’s imperative to obtain health insurance, as medical costs can consume a significant amount of your take-home earnings and savings. With the hefty premiums and other expenses, purchasing health insurance tips raises your spending substantially.

However, since purchasing the best health insurance plan raises monthly expenses overall, many people choose not to do so. You can handle this more astutely by paying attention to the health insurance tips listed below. These health insurance tips and suggestions will assist you in selecting an appropriate policy, in addition to helping you save money.

Invest in Best Health Insurance Plan at an Early Age

Purchasing a health insurance policy when you are younger can help you save money on premiums. This is due to the fact that the rate of health insurance premiums is directly correlated with the policyholder’s age. As a result, as you get older, the cost of your health insurance policy rises. This is because as you get older, you are more likely to acquire health problems, making you a bigger liability for the insurance provider. As a result, as you get older, the insurance company will charge you a higher premium.

Online Health Insurance Plan Comparison

Before making a purchase, one of the best strategies to lower your health insurance expenses is to evaluate the best health insurance plan online. You can use comparisons to get the most cost-effective health insurance plan for you without compromising on coverage. You can compare various health and general insurance services in one place using websites that let you compare them according to factors like features, coverage, and premiums.

Select a Plan That Offers Long-Term Coverage

The policy duration for most health insurance plans is one year or so. The time frame between the commencement and end dates of a health plan is referred to as the policy period in this context. When it comes to medical plans with a two- to three-year coverage length, insurers usually provide appealing discounts. In comparison to renewing the plan annually, the cumulative premium is therefore significantly lower. Consequently, these plans also shield you against inflation as they are several years long. This gives you another incentive to choose long-term plans and lowers your health insurance price.

Consider Purchasing Family Floater Health Insurance

It is necessary to purchase a family floater health insurance plan rather than individual plans for each member if you need to purchase health insurance for your entire family. As long as there is a floater sum insured, all family members are covered by a health insurance policy for family. One-time monthly premiums are required, in addition to the sum insured and insurance benefits, being divided by all insured family members. Compared to individual health insurance, this option is more cost-effective since there are no separate premiums to pay for each family member. As a result, you make significant annual savings.

All Things Considered!

Getting enough coverage from health insurance doesn’t have to be costly. The above-provided tips can help you prevent overspending on health insurance premiums. In this manner, you can safeguard yourself against unforeseen medical expenses while also saving your hard-earned money.

Term insurance and accidental insurance play a critical role in providing financial security and peace of mind to individuals and their families. It acts as a safety net in times of adversity, offering protection against unexpected events.

Term Insurance, also known as Term Life Insurance, is a type of life insurance that provides coverage for a certain period. It’s a simple and affordable life insurance that pays out a death benefit to the beneficiaries if the insured person passes away during the policy term. The policyholder receives the death benefit in a lump sum payment. Term insurance is customizable, and you can choose the policy term that works best for you. However, it doesn’t offer any investment component or cash value, and it doesn’t pay out any benefits if the policyholder survives the term. Some products provide facility like the return of premium in case the insured survives till maturity of policy.

Accidental Insurance, also called Personal Accident Insurance, is designed to provide financial coverage in the event of an accident that results in bodily injury, disability, or death. Unlike term insurance, which focuses on the risk of death, accidental insurance focuses on the risks associated with accidents namely permanent disability, partial disability and loss of pay due to

leave. Accidental insurance is more affordable than comprehensive health or life insurance policies, and many policies don’t require extensive medical underwriting. It provides coverage for specific outcomes resulting from accidents and offers benefits such as accidental death or disability.

Both term insurance and accidental are important types of insurance that provide financial protection to individuals and their loved ones in case of an unexpected event.

Comparing Term Insurance and Accidental Insurance

1. Coverage Focus:

Term Insurance: Focuses on providing a death benefit to the nominee or beneficiary in the event of the policyholder’s death due to any cause, whether it’s natural or accidental.

Accidental Insurance: Primarily covers accidents leading to bodily injury, disability, or death. It does not provide coverage for death due to natural causes or illnesses.

2. Premium Costs:

Term Insurance: Generally more affordable in terms of premium costs, making it an attractive option for individuals seeking high coverage at a lower cost.

Accidental Insurance: Typically offers lower premiums due to its specialized focus on accidental risks, but it may also provide lower coverage amounts than term insurance.

3. Benefit Payouts:

Term Insurance: Provides a lump-sum death benefit to the nominee or beneficiary upon the policyholder’s death, regardless of the cause.

Accidental Insurance: Offers benefit payouts related explicitly to accidents, such as death and disability benefits, and coverage for injuries like fractures and burns.

4. Policy Term:

Term Insurance: Typically offers a variety of policy term options, allowing you to choose the duration that best suits your needs, often ranging from 5 to 40 years or more.

Accidental Insurance: Usually comes with shorter policy terms, often renewing annually or for a few years at a time.

5. Maturity Benefit:

Term Insurance: This does not provide any maturity benefit except the return of premium if the policyholder survives the term. It is solely designed to provide a death benefit.

Accidental Insurance: Typically does not offer a maturity benefit as well, as it focuses on coverage related to accidents.

6. Medical Underwriting:

Term Insurance: Often involves a thorough medical underwriting process, which may require medical examinations and detailed health history disclosures.

Accidental Insurance: Many accidental insurance policies do not require extensive medical underwriting, making them more accessible to individuals with pre-existing health conditions.

7. Supplemental Coverage:

Term Insurance: This does not typically act as supplemental coverage for health or accidental risks. It is primarily focused on providing a death benefit.

Accidental Insurance: Often purchased as supplementary coverage alongside health or life insurance policies to address accidental risks specifically. The choice between term and accidental insurance depends on your specific financial needs, risk profile, and preferences. Choose term insurance for comprehensive coverage against natural and accidental risks, long-term protection for your family, a cost-effective solution, and a primary policy for those without existing health or life insurance. Choose the best accidental insurance plan if you want supplementary coverage for short-term needs, minimal medical underwriting, and affordable protection specifically for accidental risks. Consult with a qualified insurance advisor to help you make an informed decision. Don’t forget to review and update your insurance coverage periodically to ensure it meets your changing needs.

The Insurance Regulatory and Development Authority of India (IRDAI), which regularly monitors all insurance-related activities, strictly regulates the insurance industry in India. IRDAI launched the Point of Sales Person (POSP) project to broaden the appeal of insurance in India. To put it another way, an IRDAI accreditation enables a POSP insurance agent to sell insurance or Become a POSP Advisor.

Since there aren’t enough people with the necessary training to work as insurance agents or distributors, the penetration of insurance in India has historically been low. Even when it comes to the sale of relatively simple products like motor insurance, travel insurance, health and general insurance services, the insurance sector expects professionalism. Only registered and trained distributors can offer policies from particular insurance companies for more complex insurance products like Unit Link Insurance Plans. In order to provide insurance coverage to a larger population throughout India, the business has to hire more highly qualified insurance agents who can provide prompt and individualized customer service.

When it comes to this, the initiative to become a POSP insurance agent is crucial. The purpose of the new entry category that IRDAI has created is to speed up the process of quickly incorporating multiple insurance brokers and distributors. Compared to general agents, brokers, and corporate agents, these people have fewer strict eligibility standards. The purpose of empowering POSP insurance agents is to give them the ability to offer fundamental insurance products, especially those that require minimal documentation, explanation, or complexity.

How to become an insurance online POSP agent

Account Creation

To become a POSP advisor, you must complete this first. Visit any insurance website, click the “Become a POSP” button, provide the requested information, and create an account by entering a username and password.

KYC Document Verification

Aadhaar and PAN card copies should be uploaded as part of your KYC documentation. The insurance provider or broker will check the required documentation.

Training

A minimum of 15 hours of training is required for anyone seeking to become a POSP advisor. To begin with, you must register with an insurance provider, corporate insurance partners, or brokers. Once you become a POSP insurance agent, you are only allowed to market the goods of the insurance provider you have chosen. Only the insurance firm you hired will also give you the training and certification. Choosing the business prudently is therefore advised.

Certification Test

As we previously stated, your recruiting insurance business provides you with the certification; as a result, they also take the certification test. Prior to taking the test, you must successfully finish the training. Furthermore, online testing options are available for this exam.

All Things Considered!

In India, there is an opportunity to help make insurance more widely available by working as a point-of-sale agent. This project enables individuals to engage in insurance sales with the help of the Insurance Regulatory and Development Authority of India. Despite the fact that the procedure entails account formation, KYC document verification, training, and a certification test, it eventually gives people the ability to offer fundamental insurance products. Furthermore, in India, there is a gap in insurance coverage, and this initiative intends to fill that gap while also giving more people access to necessary coverage.

In today’s complex and unpredictable world, securing one’s financial future has become more prominent than ever before, and insurance stands out as the most effective way to mitigate financial risks. While there can be several ways to purchase insurance, individuals might have difficulty choosing a policy that caters to their requirements. This is where seeking the help of a nearby insurance advisor from a reputed broker such as Policy Ensure can aid them in choosing the right insurance. However, a person might have a prominent question: How do I find an insurance advisor near me?

When we fall sick, we consult specialist doctor. When legal matter comes we look forward to hire a specialist advocate. Similarly Insurance is a complex matter which the advisors understand better than any individual buyer. The insurance companies do not offer any discount on premium in case advisor is not there. Hence it is always better to have a nearby insurance advisor.

Policy Ensure, a pioneer in insurance brokerage services, has a wide reach in Tier 2 and Tier 3 cities, making insurance accessible to everyone. Several insurance advisors or point-of-sale persons (PoSPs) who are experts in the industry can aid a person in providing guidance, policy recommendations, claim assistance, and tailored coverage.

Multiple Insurance Companies have different products, having complex insurance jargons which is complex for any individual. It has find prints which the insurer never explains but when a claim takes place, it is denied showing one of the fine prints. Here advisors understand and ensure that broadest coverage with minimum exclusions are provided. At the same time, claim process turnaround times reduce due to involvement of an advisor due to volume being generated by the advisors.

An expert’s guidance

Insurance policies can be complex, and the industry jargon can be overwhelming for people. The local insurance advisors are well versed in the nitty-gritty of insurance and can help an individual understand terms, conditions, and exclusions in simple language. They can help people navigate through the complexities so that they get clarity about the types of insurance or health and general insurance services provided by brokers.

Policy recommendations

A lot of times, people might not know what policies will cater to their needs. Here, the insurance advisors can assess an individual’s requirements and recommend policies that align with their goals and budget. In addition, they also compare multiple coverage options, policies, and premiums to ensure a person makes informed decisions. Here, Policy Ensure makes sure that people get these local advisors at their doorsteps, so that every query is addressed and confusion is resolved.

Claims assistance

In a situation where a person requires a claim, an insurance advisor can guide them through the process while ensuring the policyholder understands every step that has been taken. They can further act as an advocate, liaising with the company on the individual’s behalf and helping them to gain the compensation they are entitled to.

Tailored coverage

Insurance does not necessarily follow a one-size-fits-all approach, and an advisor can help a person customise their coverage according to their needs. The PoSP can comprehend an individual’s unique needs and devise a coverage plan that is specifically tailored. This ensures one does not overinsure or underinsure and has the right amount of coverage for an unexpected situation. Moreover, as insurance advisers have a wide range of insurance types, one can choose the cost-effective option that can meet one’s needs.

All things considered

Insurance is an essential component of planning finances and managing risks during an unfortunate event. However, you might feel overwhelmed while choosing the right policy for your needs. This is where Policy Ensure’s PoSP can aid you with an expert’s advice, policy recommendations, claim assistance, and tailored coverage.

If you are still bothered by the question of where I can find a nearby insurance advisor, then you can rely on the wide network of Policy Ensure’s PoSPs, who are continuously striving to provide the best insurance brokerage services to people who are living in remote areas. Having an insurance advisor by one’s side can be a piece of mind, as they are ensuring that everyone is accessible to health and general insurance services provided by brokers.

For an individual, purchasing a home is one of the most vital investments. While buying a good house is important, maintaining and safeguarding it from unexpected events such as calamities or burglaries is equally critical. This is where a home insurance policy has a vital role to play. However, there can be several factors that could impact the home insurance policy cost. Therefore, before considering insurance brokerage services, it is crucial to understand the dynamics that could affect your premium. Here are five factors that are the most important:

The location of your home

The location of your home is the most critical factor in determining the cost of your home insurance policy. For instance, if you live in a high-risk area, your policy premium is likely to be high. These areas usually have a high chance of burglary or theft, making them a high-crime-rate region. On the other hand, if you are in a gated society where security measures are stringent, then the premium of your policy will be relatively low.

The characteristics of the construction

The features of the construction of your home also play a vital role in affecting your insurance premium. These characteristics include the age of the building, additional structures such as swimming pools, clubhouses, etc., and the value of these structures. The older houses have a high risk of damage and, therefore, a higher home insurance policy cost. The premiums for newly constructed houses are comparatively lower.

Weather conditions in the city

The weather conditions in your city or town are an external factor that impacts the premium on your home insurance. If you are residing in an area that is prone to natural calamities, there is a possibility that an event may damage the foundation of your home. Therefore, for people living in areas that witness regular earthquakes, floods, cyclones, and more, the cost of their insurance policy is high.

The type of insurance policy

This is the most important factor that determines the cost of your home insurance policy. Insurance is complex, and you might be paying a higher premium if you do not have the ideal policy at your disposal. This is a critical differentiator, as the insurance premiums of two similar properties can have different premiums. Therefore, it is critical to have the helping hand of the best home insurance policy advisor, who can help you choose the right policy for your house, saving you a substantial amount of money.

Safeguard your home with Policy Ensure

Choosing the best home insurance for your house can be a daunting task. This is where Policy Ensure can extend a helping hand. Being a pioneer in insurance brokerage services, Policy Ensure provides you with a myriad of options to choose from. Furthermore, to simplify your search, you also have a provision to consult the best home insurance policy advisor, who is a point of sale person (PoSP). They can guide you through the whole process of choosing and then purchasing the ideal policy for your needs.

The wide network reach ensures that the PoSPs reach your doorstep and explain all the above-mentioned factors that could impact home insurance policy costs. As a result, you safeguard your house in case of any unexpected events while saving a huge amount on the premium. A house is a dream for many people; therefore, protect it with home insurance today.

Living in a fast-paced world has become increasingly stressful, which is impacting the health of many people, especially in India. According to a large-scale survey by Statista, almost 61% of Indian women and 47% of Indian men were unhealthy based on their diet and lifestyle choices. Therefore, having the best health insurance premiums plan has become crucial in a bid to manage the rising healthcare costs.

Today, there are several insurance plans available for you and your family. However, the policies may differ on several aspects, such as premiums, benefits, coverage, and more. It can be a possibility that you might be paying a higher premium if you do not have the right knowledge and information. In this piece, we will discuss how you can save money on premiums and get the best affordable health insurance.

Start early

One can get several benefits from purchasing health insurance at an early age, as the premium for health insurance increases with age. In other words, the rate of the health insurance premium is directly proportional to the age of the policyholder. This is due to the fact that people are more susceptible to diseases as they age. Therefore, the premiums will cost less at your young age owing to the lower risk to the insurance companies.

Buy insurance for the entire family.

Another way to save money for an individual is to purchase a health insurance policy for family instead of buying individual plans for each member. A family health insurance plan provides coverage on a floated-sum insured basis. The benefit of this floater plan is that all the family members share its benefits, and you only need to pay a single premium amount. Thus, it leads to huge cost savings on premiums.

Go for long-term tenure.

The long-term tenure of a health insurance policy can help you save on premiums. Typically, plans that come with a tenure of two or three years are less expensive than one-year plans. Therefore, you get the best affordable health insurance with a long-term policy discount, which also saves the hassle of renewing the policy every year.

Choose the coverage wisely

In order to save on the premium you are going to pay, you must choose the coverage with the utmost care. However, the terminology of insurance can be overwhelming for some people, and choosing the best health insurance plan can become difficult. This is where consulting a licenced insurance broker, such as Policy Ensure, can be the best option. Their insurance advisors or point-of-sale people (PoSP) can comprehend your needs and help you choose the coverage by suggesting the most affordable health insurance for you.

Lead a healthy life with Policy Ensure

Having health insurance has become crucial in today’s time and age, whether you are purchasing one for yourself or a health insurance policy for family. However, in a bid to save money on health insurance premiums, one must purchase a policy at a young age, buy a floater plan for the family, consider a long-term tenure plan, and choose the coverage wisely.

For some people, purchasing the best health insurance plan can be daunting, but fortunately, licenced brokers such as Policy Ensure are here to help. You can reach out to a PoSP, who will understand your requirements and then suggest the best insurance policy that is affordable for you. This is how a broker can help you future-proof your health in a hassle-free and convenient manner.

World Heart Day is celebrated by organizing various activities and awareness events globally to raise awareness about heart disease and its preventive measures to manage cardiovascular diseases. Here are 4 startups working towards making a difference.

The day is celebrated by organizing various activities and awareness events globally to raise awareness about heart disease and its preventive measures to manage cardiovascular diseases. The events mainly focus on educating people about the signs and symptoms of cardiovascular disease to avoid any further complications and encouraging people to inculcate a healthy lifestyle to prevent and control any heart-related ailments.

The heart is one of the vital organs of the human body, malfunctioning of it may lead to fatality, so everyone needs to take care of heart health. Due to a lack of awareness about cardiovascular health and certain lifestyle habits, cardiovascular diseases (CVDs) is one of the leading reason for mortality worldwide. Every year, around 1.7 crores people die due to cardiovascular disease, accounting approx 31% of all global mortality.

Heart attack, Stroke and coronary heart disease are some of the most common reasons of death due to cardiovascular disorders. These heart disorders account for nearly 85% of total deaths due to cardiovascular ailments. World Heart Day plays a vital role in creating awareness to educate people across the world to understand the importance of heart health and bringing other organizations together to actively participate in organizing various events to create awareness. Here are 4 startups working towards making a difference.

1. Policy Ensure

Policy Ensure promotes heart-healthy lifestyles by offering health insurance policies that incentivize regular health check-ups, provide coverage for preventive care, and offer discounts on fitness memberships. Rahul M Mishra, Co-Founder and Director, of Policy Ensure shared, “Our educational resources emphasize the importance of exercise, balanced diets, and stress management for overall heart health.” Mental health support and preventive care for chronic diseases often receive insufficient attention in healthcare. “Healthcare disparities in underserved communities need addressing to ensure equitable access to quality care,” he added.

2. Kapiva

Dr Kriti Soni, Head of R&D at Kapiva explained, “At the core of Kapiva, we are committed to catering to overall health and wellness including heart health. We offer products featuring heart-healthy herbs and Ayurveda-approved supplements and endorse stress-reducing practices like yoga and meditation. These holistic approaches align with Ayurvedic principles to empower individuals to achieve lasting heart wellness through balanced living”. She further added, “Many aspects of healthcare tend to be overlooked by the general public. These often neglected areas encompass mental health, preventive care, the management of chronic diseases, and the consideration of social determinants of health. For example, herbs like Ashwagandha help keep stress levels in check, or Cinnamon to keep blood lipid levels like LDL cholesterol in control.” “The goal is to control blood pressure for optimal heart health through Ayurvedic solutions,” she said.

3. KITES Senior Care

Dr Reema Nadiq the Co-Founder and Group Medical Director explained, “We prioritize heart health of our elderly. We promote active and healthy lifestyles in our retirement homes and also at their residences, emphasizing physical and mental well-being, which plays a vital role in heart health as we age.” Parallelly they will soon be launching a remote health tech platform. This innovative solution will enable us to closely monitor the heart health of active seniors, providing real-time support and interventions to ensure their continued well-being and a healthier, happier life.

4. Dozee

CEO and Co-founder, Mudit Dandwate shared, “There is a growing need for the continuous monitoring of cardiac health to prevent cardiovascular diseases and sudden heart failures and heart attacks. Taking into account the fact that undetected cardiac anomalies might fatally affect patients, the utilization of AI-based continuous monitoring technology can enable healthcare providers with early detection and timely intervention.” To that end, Dozee’s AI-based remote patient monitoring (RPM) and early warning system (EWS), developed with the usage of 150-year-old Ballistocardiography (BCG) technology can efficiently monitor the cardiac activity of individuals with clinical grade precision and accuracy. By continuously tracking parameters such as blood pressure, heart rate/pulse rate, SpO2, respiration rate and temperature, we offer a comprehensive solution for continuous cardiac health monitoring, allowing healthcare providers to intervene timely and prevent cardiovascular diseases, sudden heart failures, and heart attacks.

Uncertainties, accidents, and unannounced events are an inevitable part of life and there is no escape from it. From major mishaps to minor injuries, accidents not only take a toll on our physical and mental well-being but also have a significant financial impact. While you might assume that your existing term and health insurance policies provide sufficient coverage, it is crucial to have a personal accident insurance policy.

Due to the simple reason that a life insurer only provides financial security in the event of the policyholder’s death, personal accident insurance is essential. In fact, accidents can result in both temporary and permanent disabilities, leading to loss of income and additional medical expenses. The best accidental insurance policy not only provides coverage in case of death but also offers vital financial protection for you and your family in the event of an accident. Whether it is a major incident like a car crash or a minor mishap like falling off a bicycle or fracturing an arm, these policies cover a wide range of scenarios, making them essential for individuals. While an accident cannot be prevented from causing stress, trauma, and physical and mental suffering, one can prepare to mitigate financial instability through individual personal accident insurance. Finding the greatest accidental insurance plan or policy, however, can be a difficult endeavor. Assisting people in locating coverage that meets their unique needs while saving them time and effort, insurance advisors play a crucial role.

What is covered by personal accident insurance?

Total temporary disability: Under this, the policyholder becomes eligible for weekly compensation for incidents that restrict them for up to certain weeks until they recover, such as fractures to the hands or legs.

Partial permanent disability: In this case, the policyholder receives a small portion of the sum assured at weekly or monthly intervals. Losing a finger or an entire hand, etc., are all considered partial permanent disabilities under this provision.

Total permanent disability: In cases of total permanent disability, a specified percentage of the sum insured is paid to the policyholder.

Accidental death and transportation of mortal remains: If the policyholder passes away unexpectedly, the insurer will pay the nominee the full amount insured as well as a predetermined amount for the transportation of the deceased.

Educational benefit: The policy covers the expense of up to two dependent children up to the age of 23.

Key policy perks

Financial support for the family of deceased: There is no denying the fact that accidents come unannounced and can take place anytime and anywhere, resulting in sudden death. As a result, the family of the deceased is put under a great deal of financial strain, which puts them in a terrible situation. However, if a person has an accident insurance policy and is involved in an accident that kills them, the nominee they choose will receive 100% of the designated insured sum in compensation. Thus, in such instances, having individual personal accident insurance considerably supports the policyholder’s family in overcoming financial obstacles.

Offering monetary assistance to the policyholder: A person may experience a permanent or temporary impairment as a result of terrible accidents, which could result in a loss of income. Here an accidental insurance policy plays a crucial role in providing the policyholder with financial compensation based on the type of disability. This makes sure the victim is protected in the case of a permanent disability or if a temporary disability develops into a permanent one. Therefore, it is essential to select the best accidental insurance policy in order to stay safe while having financial support at your doorstep as and when required and find the best car and motor insurance services.

Covers hospital and ambulance charges: In certain instances, a person may experience an accident at a specific site, yet he or she might end up being treated in a hospital that is located elsewhere. Under such circumstances, the concerned individual’s accidental insurance will play an important part in covering the transportation expenses, sparing the family from incurring huge expenditure. Moreover, the policy covers a portion of hospital care and post-hospitalization costs, providing the policyholder with much-needed respite. In addition, the affected person gets the best possible coverage for their education, work benefits, and funeral costs.

Personal accident insurance: Solution to uncertainties

Life is undoubtedly God’s most priceless gift, and nothing is more valuable than that. Thus, it is imperative that we as individuals take appropriate measures to safeguard our lives and the lives of our loved ones. With the best accidental insurance policy, the insured and concerned loved ones will be able to derive necessary benefits in the event of extreme occurrences such partial or permanent disability, and sudden death. Thus, if you still have not yet secured a dedicated accident insurance plan, it is advisable to consult with a reputable insurance broker to obtain one without any further delay.

Health Insurance for Diabetes and BP patient अगर कोई डायबिटीज और बीपी का रोगी सस्ती दर पर हेल्थ इंश्योरेंस लेना चाहता है तो उसे अपनी जीवनशैली में बदलाव करना होगा। इसके साथ बीमा कराते समय रिसर्च और नो क्लेम बोनस का फायदा लेकर भी डायबिटीज और बीपी का रोगी कम प्रीमियम पर हेल्थ इंश्योरेंस पॉलिसी ले सकता है।

नई दिल्ली, बिजनेस डेस्क। डायबिटीज और बीपी के रोगियों के लिए स्वास्थ्य बीमा आम लोगों के मुकाबले काफी महंगा होता है। एक्पर्ट्स बताते हैं कि अगर सही तरीके अपनाएं जाए तो डायबिटीज और बीपी रोगियों को भी स्वास्थ्य बीमा किफायती दरों पर मिलता है।

बीमा क्षेत्र में काम करने वाली कंपनी पॉलिसी एनश्योर के सह-संस्थापक और निदेशक, राहुल एम मिश्रा का कहना है कि अगर कोई डायबिटीज और बीपी से ग्रस्ति व्यक्ति कम दर पर स्वास्थ्य बीमा चाहता है तो उसको कुछ तरीकों को जरूर अपनाना चाहिए।

1.नियमित स्वास्थ्य जांच: बीमा कंपनियों को अपनी नियमित रूप से अपनी जांच रिपोर्ट और स्वास्थ्य स्थिति प्रदर्शित करनी चाहिए। साथ ही आपको अपनी जांच रिपोर्ट्स का पूरा रिकॉर्ड रखना चाहिए।

2. तुलनात्मक खरीदारी: आपकी आवश्यकताओं और बजट के लिए सबसे उपयुक्त बीमा पॉलिसी खोजने के लिए विभिन्न बीमाकर्ताओं की स्वास्थ्य बीमा पॉलिसियों पर रिसर्च करें और उनकी तुलना करें।

3.विशिष्ट योजनाएं: विशेष रूप से पहले से मौजूद बीमारियों वाले व्यक्तियों के लिए डिजाइन की गई स्वास्थ्य बीमा योजनाओं की तलाश करें। कुछ बीमाकर्ता डायबिटीज और बीपी की विशिष्ट योजनाएं पेश करते हैं।

4.समूह बीमा: यदि आप कार्यरत हैं, तो जांचें कि क्या आपका नियोक्ता समूह स्वास्थ्य बीमा प्रदान करता है। ये पॉलिसियां अक्सर बेहतर कवरेज और कम प्रीमियम प्रदान करती हैं।

5.जीवनशैली में बदलाव: स्वस्थ जीवनशैली में बदलाव करना जैसे कि अपना वजन नियंत्रित करना और नियमित व्यायाम करना। आपकी हेल्थ पॉलिसी का प्रीमियम कम करने में मदद कर सकता है।

6.नो क्लेम बोनस: ऐसी पॉलिसियां चुनें जो नो क्लेम बोनस (एनसीबी) प्रदान करती हैं। आप प्रत्येक दावा-मुक्त वर्ष के लिए sum insured enhancement अर्जित कर सकते हैं।

7.सरकारी योजनाएं: आयुष्मान भारत जैसी सरकार प्रायोजित स्वास्थ्य बीमा योजनाओं का पता लगाएं, जो पहले से मौजूद कुछ स्थितियों के लिए कवरेज प्रदान कर सकती हैं।

8.बीमा सलाहाकार: बीमा सलाहाकार से परामर्श करने पर विचार करें जो आपकी विशिष्ट स्वास्थ्य आवश्यकताओं के अनुरूप सबसे अधिक लागत प्रभावी पॉलिसी ढूंढने में आपकी सहायता कर सकता है।

स्टार हेल्थ मधुमेह सुरक्षित बीमा: विशेष रूप से मधुमेह रोगियों के लिए डिजाइन किया गया, यह मधुमेह से उत्पन्न होने वाली जटिलताओं को कवर करता है।

एचडीएफसी एर्गो स्वास्थ्य सुरक्षा गोल्ड: व्यापक कवरेज प्रदान करता है और इसमें प्रतीक्षा अवधि के बाद पहले से मौजूद स्थितियों के लिए कवरेज शामिल है।

मैक्स बूपा हेल्थ कंपेनियन: आजीवन नवीकरणीयता प्रदान करता है और प्रतीक्षा अवधि के बाद पहले से मौजूद स्थितियों को कवर करता है।

अपोलो म्यूनिख ऑप्टिमा रिस्टोर: यदि पॉलिसी वर्ष के दौरान बीमा राशि समाप्त हो जाती है तो उसे बहाल करने की एक अनूठी सुविधा प्रदान करता है।

न्यू इंडिया एश्योरेंस मेडिक्लेम पॉलिसी: पहले से मौजूद स्थितियों के लिए कवरेज वाली पॉलिसी प्रदान करती है, हालांकि प्रतीक्षा अवधि लागू हो सकती है।

Only 25 per cent of Indians going abroad buy travel insurance well in advance while making travel arrangements; a large majority wait until the last 3 days to buy it, according to a survey conducted by Policybazaar.

While people nowadays understand the importance of buying travel insurance, they are still not aware of the lesser-known benefits of buying one, besides coverage for baggage loss, flight cancellation and medical emergencies. This could also be because, predominantly, a major chunk of Indian travellers go to Asian countries, and they don’t need to present their policy copy until the day of the trip.

As of July 2023, over 38 per cent of the people travelling abroad planned their trip for more than 15 days, mostly for European countries, followed by 26 per cent planning to stay for 7-10 days.

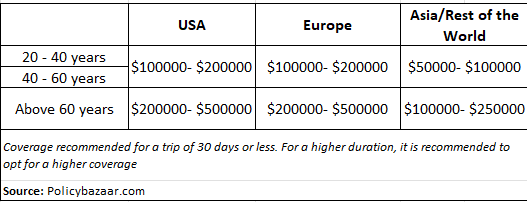

Seven out of 10 people understand the importance of having an adequate sum insured while travelling abroad, choosing over $100,000 as sum insured. The rest of them choose almost half of it, which is the minimum coverage you can opt for, according to the survey.

The trend of vacationing abroad has reached the pre-pandemic level, with over 97 per cent of people currently travelling outside the country for leisure. Thailand continues to be the most preferred Asian travel destination for Indians. Vietnam and Indonesia are also emerging as hot travel destinations after the pandemic.

“Just like you plan your accommodation, flights and itinerary, deciding on a comprehensive travel insurance policy that can protect and safeguard you against common travel inconveniences is essential, allowing you to peacefully enjoy your trip with family. Before buying a travel insurance policy, you must check all the inclusions and exclusions carefully. You must ensure that the most common and basic benefits like coverage for Covid-19, medical emergencies, trip cancellation and curtailment, baggage loss and passport theft, etc, are covered under your policy,” said Manas Kapoor, Product Head – Travel Insurance, Policybazaar.com.

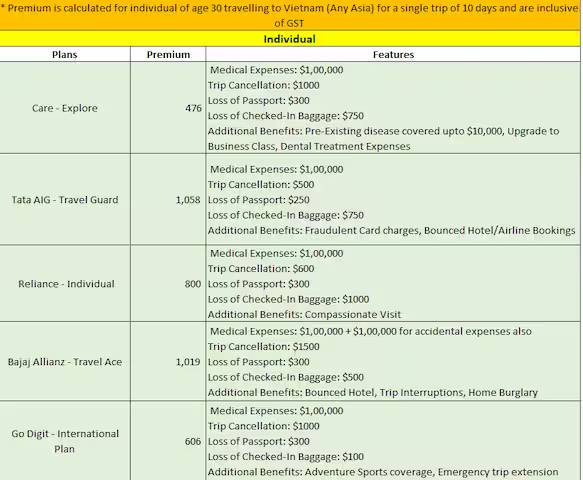

Some other popular benefits that travellers should opt for are coverage for pre-existing diseases or illnesses, OPD coverage, trip extensions, personal accident cover, home burglary insurance and multi-trip insurance or frequent flyers plan. Policybazaar has curated a list of travel insurance policies available for overseas trips to Asia that you can opt for

How to choose the right travel insurance policy when travelling overseas:

Rahul Meena Mishra, co-founder & director, Policy Ensure, explains how to choose and decide on your travel policy:

• Assess your needs: Consider your travel destination, duration, and activities you plan to engage in. Determine the level of coverage you require for medical emergencies, trip cancellation or interruption, baggage loss, and personal liability.

• Check coverage limits: Review the coverage limits provided by different insurance policies. Ensure they meet your specific requirements, especially for medical expenses, emergency medical evacuation, and trip cancellation costs.

• Understand exclusions: Read the policy exclusions carefully. Be aware of situations or activities that may not be covered, such as pre-existing medical conditions, adventure sports, or acts of terrorism. If you need coverage for any excluded items, look for policies that offer optional add-ons or specialised coverage.

• Medical coverage: Pay close attention to the medical coverage offered by the policy. Check if it includes emergency medical treatment, hospitalisation, ambulance services, and repatriation of remains. Ensure the coverage limits are sufficient for the destination you’re visiting, as healthcare costs can vary widely across countries.

• Trip cancellation and interruption: If your trip is expensive or involves non-refundable bookings, consider a policy that provides comprehensive trip cancellation and interruption coverage. This will protect you financially in case unforeseen circumstances force you to cancel or cut short your trip.

• Baggage and personal belongings: Look for a policy that offers coverage for lost, stolen, or damaged baggage and personal belongings. Check the coverage limits and any sub-limits for valuable items like electronics or jewellery. Also, verify if the policy covers delayed baggage and provides reimbursement for essential items during the delay

• Compare prices and reviews: Obtain quotes from multiple insurance providers and compare the prices against the coverage offered. However, remember that the cheapest policy may not always provide the best coverage or customer service. Read reviews and ratings of the insurance company to gauge its reputation and customer satisfaction level.

• Pre-existing medical conditions: If you have pre-existing medical conditions, ensure that the policy covers them or offers a waiver for pre-existing conditions. Some policies may require you to declare your medical conditions upfront or undergo a medical examination.

• Travel assistance services: Consider the additional services provided by the insurance company, such as 24×7 emergency assistance, travel concierge services, or language translation support. These can be valuable during emergencies or if you need assistance while travelling.

What’s the ideal option and cover? Overview of the right coverage based on age and destination, according to policybazaar:

Destination-specific coverage: Different countries may have unique risks and healthcare systems. Research the healthcare facilities, quality of care, and associated costs in the countries you intend to visit.

Schengen Visa requirements: If you’re travelling to Schengen countries in Europe, it is mandatory to buy travel insurance that meets the minimum coverage requirements (30,000 euros) specified by the Schengen visa authorities. Make sure your chosen policy fulfils these requirements to avoid any issues with your visa application.

High-cost destinations: Some countries, such as the United States, Canada, or countries in Western Europe, have higher healthcare costs. If you plan to visit these destinations, ensure your travel insurance policy offers sufficient coverage for medical expenses to avoid potential financial burdens.

Adventure sports and activities: If you’re planning to engage in adventure sports or activities like skiing, scuba diving, or bungee jumping, check if your policy covers such activities. Some policies may have exclusions or require additional coverage for high-risk activities.

Political unrest and natural disasters: If you’re travelling to regions with a history of political unrest or natural disasters, consider a policy that includes coverage for trip cancellation, trip interruption, or evacuation due to these unforeseen events.

Duration of travel: If you’re a frequent traveller or planning a long-term trip, look for policies that offer coverage for extended periods. Some policies may have limitations on the maximum duration of coverage, so choose one that aligns with your travel plans.

Family coverage: If you’re travelling with family members, especially children or elderly individuals, ensure the policy provides suitable coverage for their specific needs. This may include coverage for pediatric care, pre-existing conditions, or medical evacuation for older travellers.

Policy extensions and renewals: If you’re planning to extend your trip or have flexible travel plans, check if your insurance policy allows for extensions or renewals while you’re abroad. It’s important to have continuous coverage throughout your entire trip.

“To maximise the protection, ensure coverage for checked-in baggage loss, trip delay/cancellation, and loss of passport. An emergency cash assistance feature in the policy can be useful if you are mugged or robbed on foreign soil and left without travel funds. It will also be prudent to have a personal liability feature that covers legal liability to a third party resulting in injury, damage to property, and even death, during your trip,” said Rakesh Jain, CEO of Reliance General Insurance.